These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

If you can swing this, it makes good sense. Why? Interest on your student loan accrues daily. Just cut your monthly payment in half and make two payments per month. This way, it might be easier to juggle your finances, as opposed to doling out one big chunk every month. Also, paying more often gives you the feeling that you’re making progress – and you are because of the daily accrual. #WinWin

Use the Debt Avalanche Method

With this approach, you’re paying off your highest interest debt first. Makes sense, right? After you do this, make minimum payments on all of your other loans. If you have any extra cash left over, pay your highest interest loan. Keep at this until you’re paid in full.

Claim the Student Loan Tax Deduction

This is cool. You can write off up to $2,500 of your student loan interest. Now, the amount you can write off depends on your income because there are phaseouts and gradual reductions in place. Just use the 1098-E form (you can get this from your loan servicer) to figure out how much interest you’ve paid. Then get going.

Pay While Still in School

Talk about getting a head start.You’ll cut down on interest (a good thing) while forgoing in-school deferment, and start paying down your debt pronto.

Pay Off Private Student Loans First

Should you have public and private student loans, this is the best strategy. Here’s why: private loans don’t offer student loan forgiveness or income-driven repayment. And they have limited deferment options. You’ll be better off doing this, given all the stipulations that exist for these kinds of loans.

Use Employer Repayment Assistance Programs

This is a sweet deal. Check with your employer to see if they offer such a program. Generally, they offer reimbursement or allocate funds to help you. Don’t forget to ask!

Pay During the Grace Period

This is the six-month period after graduation. While this might not be something that’s initially appealing, think it through. It helps keep interest in check and prevents your balance from growing during your grace period. Also, starting earlier means you’ll finish earlier. Gotta love that.

Consolidate Federal Student Loans

This is a great idea for those with limited resources. You can lower your payment and extend the repayment terms. You’ll most likely pay more interest, but for a short-time solution it’s a good one.

Exceed the Minimum Payment

If you have the means to make this happen, by all means, do it. Another great way to make incredible progress is to make double payments. If you can’t pay double, at least try to pay over the required amount. It’ll help eat away at the interest and eventually, the principal.

Student loans are great while you’re in school, right? They enable you to get the education you want. And while paying them off might be overwhelming, if you use these methods, you’ll be ahead of the game and pay them off sooner than you think.

November 1, 2021 · Blog, Tip of the Month, Uncategorized

⏱ 4 min read

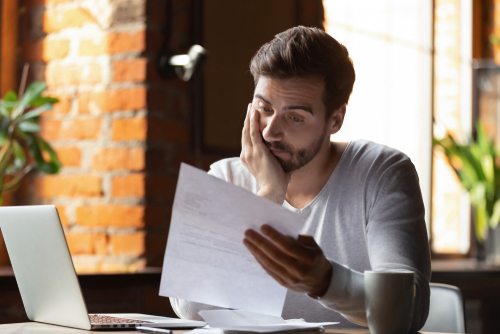

If the thought of paying off your student loan causes a bit of anxiety, worry no more. Here are some ways to pay it off faster. Check them out.

Sign Up for Auto-Pay

This might seem like the most obvious thing to do, and yet, some alums don’t take full advantage of it. The psychology of this works well. When you decide to put your payment on auto-draft, you never miss it. You get used to living on a certain amount of money. Better still, there are lenders who offer refinancing at lower rates, ranging from 1.8 percent to 7.84 percent. But there’s more: Some lenders offer cash-back bonuses. With that said, the catch is you give up important benefits like income-driven repayment and student loan forgiveness. However, refinancing can help you save a bunch – like thousands of dollars.

Pay Bi-Weekly

If you can swing this, it makes good sense. Why? Interest on your student loan accrues daily. Just cut your monthly payment in half and make two payments per month. This way, it might be easier to juggle your finances, as opposed to doling out one big chunk every month. Also, paying more often gives you the feeling that you’re making progress – and you are because of the daily accrual. #WinWin

Use the Debt Avalanche Method

With this approach, you’re paying off your highest interest debt first. Makes sense, right? After you do this, make minimum payments on all of your other loans. If you have any extra cash left over, pay your highest interest loan. Keep at this until you’re paid in full.

Claim the Student Loan Tax Deduction

This is cool. You can write off up to $2,500 of your student loan interest. Now, the amount you can write off depends on your income because there are phaseouts and gradual reductions in place. Just use the 1098-E form (you can get this from your loan servicer) to figure out how much interest you’ve paid. Then get going.

Pay While Still in School

Talk about getting a head start.You’ll cut down on interest (a good thing) while forgoing in-school deferment, and start paying down your debt pronto.

Pay Off Private Student Loans First

Should you have public and private student loans, this is the best strategy. Here’s why: private loans don’t offer student loan forgiveness or income-driven repayment. And they have limited deferment options. You’ll be better off doing this, given all the stipulations that exist for these kinds of loans.

Use Employer Repayment Assistance Programs

This is a sweet deal. Check with your employer to see if they offer such a program. Generally, they offer reimbursement or allocate funds to help you. Don’t forget to ask!

Pay During the Grace Period

This is the six-month period after graduation. While this might not be something that’s initially appealing, think it through. It helps keep interest in check and prevents your balance from growing during your grace period. Also, starting earlier means you’ll finish earlier. Gotta love that.

Consolidate Federal Student Loans

This is a great idea for those with limited resources. You can lower your payment and extend the repayment terms. You’ll most likely pay more interest, but for a short-time solution it’s a good one.

Exceed the Minimum Payment

If you have the means to make this happen, by all means, do it. Another great way to make incredible progress is to make double payments. If you can’t pay double, at least try to pay over the required amount. It’ll help eat away at the interest and eventually, the principal.

Student loans are great while you’re in school, right? They enable you to get the education you want. And while paying them off might be overwhelming, if you use these methods, you’ll be ahead of the game and pay them off sooner than you think.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

To avoid the challenges mentioned above, you should automate the accounts payable process.

Accounts Payable Automation

Automation removes slow and repetitive manual tasks and lets you digitally submit and approve purchase orders and invoices.

However, when making any investment, businesses are more concerned about the return on investment (RIO). Rest assured that through automation, you can achieve ROI through reduced employment costs, fewer late fees, savings on invoice processing costs, and reduced losses caused by errors, among other non-financial benefits.

Following are the benefits achieved by streamlining the accounts payable workflow through automation:

Get a more accurate picture of your finances – using automation software gives you access to reporting capability that makes it is easy to get a quick overview of business spending.

Have a better command over cash flow – manage cash better with the help of reports that can be created and reviewed in real-time, which improves AP team visibility and forecasting. Automation will help in invoice prioritization as well.

Improve user productivity – employees do not have to waste time sorting documents. With the data centrally stored, employees only need to run a query to find the necessary invoice or purchase order.

Enable remote work – using cloud-based software makes remote access possible and enables approvals to be done remotely.

Auditing is easy – all data is stored in a central database and can be easily accessed.

Cost-effective – it enables timely payments and helps avoid unnecessary penalties and interest fees.

Reduce overhead staff costs – automation will help reduce the accounts payable team, with no need to hire more staff even when a business grows.

Dashboard and analytics tools – allow access to separate dashboards for the team and approvers, each using individual login credentials. At the same time, analytics gives a quick overview of the whole process.

No manual data entry – scan documents to capture data and avoid manual data entry.

Standardized accounts payable workflow – ensures consistency even if your business has different teams responsible for handling the invoicing data.

Payment reminders – set your system to have reminders when pay dates are near. This will help avoid late or forgotten payments.

Qualify for discounts – with a smooth workflow, the accounts payable cycle will require less time, and you may qualify for discounts from suppliers for early payments.

Conclusion

A disorganized accounts payable process can run your business down. Choosing the right AP automation software will help improve accuracy, efficiency, quality and speed for your business accounts payable function. Your business also will have a balance between a healthy cash flow and, at the same time, maintaining a good supplier relationship.

Why you should automate your accounts payables

November 1, 2021 · Blog, Uncategorized, What’s New in Technology

⏱ 4 min read

Accounts payable (AP) is a crucial function to any business, as errors in the process put a company in problems. Although many businesses still use manual methods as they find the system to work fine, it requires a lot of precision from the accounts payable team. There are better – and more efficient – ways to manage AP through automation.

Challenges of the Process

An AP team is responsible for receiving invoices, reviewing invoices, approving invoices, and paying suppliers and vendors. Some AP departments also handle other functions, depending on the nature of the business. However, AP can be a time-consuming, strenuous and paper-intensive process.

An AP team helps a business control costs, maintain a good supplier relationship and analyze spending. Various challenges might indicate that your business is using outdated practices. Such challenges might include:

Dealing with double payments

Difficulties in tracking invoices, especially when your business has many transactions

Forgotten payments

Fraud

Disappearing invoices

Missing purchase orders

Poor business reputation as suppliers lose trust in your business

Negative cash flow

Too much paperwork taking up employees’ time to sort and organize

Skipped processes

Manual processes that result in errors and delays

These challenges not only affect your business negatively, but they also affect your supplier’s business. Consider that late payments cost small businesses $3 trillion per year, which means your late payments create a domino effect. Your business will also be subjected to late payment fines.

To avoid the challenges mentioned above, you should automate the accounts payable process.

Accounts Payable Automation

Automation removes slow and repetitive manual tasks and lets you digitally submit and approve purchase orders and invoices.

However, when making any investment, businesses are more concerned about the return on investment (RIO). Rest assured that through automation, you can achieve ROI through reduced employment costs, fewer late fees, savings on invoice processing costs, and reduced losses caused by errors, among other non-financial benefits.

Following are the benefits achieved by streamlining the accounts payable workflow through automation:

Get a more accurate picture of your finances – using automation software gives you access to reporting capability that makes it is easy to get a quick overview of business spending.

Have a better command over cash flow – manage cash better with the help of reports that can be created and reviewed in real-time, which improves AP team visibility and forecasting. Automation will help in invoice prioritization as well.

Improve user productivity – employees do not have to waste time sorting documents. With the data centrally stored, employees only need to run a query to find the necessary invoice or purchase order.

Enable remote work – using cloud-based software makes remote access possible and enables approvals to be done remotely.

Auditing is easy – all data is stored in a central database and can be easily accessed.

Cost-effective – it enables timely payments and helps avoid unnecessary penalties and interest fees.

Reduce overhead staff costs – automation will help reduce the accounts payable team, with no need to hire more staff even when a business grows.

Dashboard and analytics tools – allow access to separate dashboards for the team and approvers, each using individual login credentials. At the same time, analytics gives a quick overview of the whole process.

No manual data entry – scan documents to capture data and avoid manual data entry.

Standardized accounts payable workflow – ensures consistency even if your business has different teams responsible for handling the invoicing data.

Payment reminders – set your system to have reminders when pay dates are near. This will help avoid late or forgotten payments.

Qualify for discounts – with a smooth workflow, the accounts payable cycle will require less time, and you may qualify for discounts from suppliers for early payments.

Conclusion

A disorganized accounts payable process can run your business down. Choosing the right AP automation software will help improve accuracy, efficiency, quality and speed for your business accounts payable function. Your business also will have a balance between a healthy cash flow and, at the same time, maintaining a good supplier relationship.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Stock buybacks have had a significant impact on the markets. Not only are companies using excess cash to buy back shares, but with interest rates so low for so long, many companies have even taken on debt to buy back shares. Still, excess cash that can’t just sit on the corporate balance sheet is the main driver of the largest buyback programs. Established, cash-flush tech companies such as Apple, Alphabet and Microsoft are the dominant players, accounting for nearly one-third of all buyback activity in the first half of 2021.

Given the recent run-up in the markets, buyback programs have not kept up. Couple this with the proposed increases in corporate tax rates from 21 percent to 25 percent, and there’s even less cash to fund buyback programs. Generally, most experts believe these macro-economic factors combined with the new 2 percent tax will cause a shift toward dividend payouts as they will be more favorable to shareholders.

Conclusion

The main idea behind the proposed 2 percent excise tax on stock buybacks is to both raise revenue and encourage corporate investment. Critics of stock buyback programs believe this is better for the economy and workers, whereas buybacks favor corporate shareholders at their expense. While a 2 percent tax might not be enough to create wholesale change, it appears to have enough teeth combined with corporate tax rate changes to change most public company CFOs.

Potential New Tax on Stock Buybacks and What it Could Mean for the Financial Markets

November 1, 2021 · Blog, Tax and Financial News, Uncategorized

⏱ 3 min read

President Biden’s latest spending bill could result in a new tax on corporate stock buybacks. In its most recent incarnation, the Senate version of the plan includes a 2 percent excise tax on stock buybacks. Still, this isn’t enough for many critics of stock buybacks, who claim they incentivize short-term behavior in lieu of long-term investment.

Short-Term Incentives

Stock buyback programs have long been criticized for giving a short-term boost to share prices with funds that could have been used for long-term investment instead. Critics, including the current president, believe stock buybacks come at the expense of capital investment in new or updated factories, research, worker training, etc. These critics believe this type of long-term investment is the key to sustainable growth.

Changing Behavior with Taxes

Some critics advocate for an outright ban on stock buybacks, but they are in the minority. Instead, the recent Senate bill proposes a 2 percent tax on stock buybacks. This tax is dual purpose. First, it aims to discourage buybacks and encourage longer-term investment. Second, it’s a revenue generator to help fund the trillions in new spending in the bill.

Will the 2 Percent Tax be Enough to Matter?

While a 2 percent excise tax on buybacks may not be draconian, it appears to be significant enough to drive a change in behavior. In a CNBC poll, more than half of CFOs indicated the 2 percent tax is enough for them to curtail their buyback program. Only 40 percent said they would not change their buyback program plans (CNBC Global CFO Council Survey).

Impact on the Capital Markets

Stock buybacks have had a significant impact on the markets. Not only are companies using excess cash to buy back shares, but with interest rates so low for so long, many companies have even taken on debt to buy back shares. Still, excess cash that can’t just sit on the corporate balance sheet is the main driver of the largest buyback programs. Established, cash-flush tech companies such as Apple, Alphabet and Microsoft are the dominant players, accounting for nearly one-third of all buyback activity in the first half of 2021.

Given the recent run-up in the markets, buyback programs have not kept up. Couple this with the proposed increases in corporate tax rates from 21 percent to 25 percent, and there’s even less cash to fund buyback programs. Generally, most experts believe these macro-economic factors combined with the new 2 percent tax will cause a shift toward dividend payouts as they will be more favorable to shareholders.

Conclusion

The main idea behind the proposed 2 percent excise tax on stock buybacks is to both raise revenue and encourage corporate investment. Critics of stock buyback programs believe this is better for the economy and workers, whereas buybacks favor corporate shareholders at their expense. While a 2 percent tax might not be enough to create wholesale change, it appears to have enough teeth combined with corporate tax rate changes to change most public company CFOs.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Did you know that homeowner’s insurance doesn’t cover flood damage? Because of this, homes located in a Special Flood Hazard Area (SFHA) are required by lenders to purchase a separate flood insurance policy. However, there are millions of homes at risk that also experience periodic flooding but are not located in the most hazardous zones.

Did you know that homeowner’s insurance doesn’t cover flood damage? Because of this, homes located in a Special Flood Hazard Area (SFHA) are required by lenders to purchase a separate flood insurance policy. However, there are millions of homes at risk that also experience periodic flooding but are not located in the most hazardous zones.